Have Questions?

Call Us at 210-495-5626

Have Questions?

Call Us at 210-495-5626

A FICO Score is a three-digit number based on the information in your credit reports. It helps lenders determine how likely you are to repay a loan. This, in turn, affects how much you can borrow, how many months you have to repay, and how much it will cost (the interest rate). Below is a chart that breaks down how your scores are viewed compared to the average U.S. consumer.

| FICO Score Ranges | Rating | Description |

| <580 | Poor | Your score is well below the average score of U.S. consumers and demonstrates to lenders that you are a risky borrower. |

| 580-669 | Fair | Your score is below the average score of U.S. consumers, though many lenders will approve loans with this score. |

| 670-739 | Good | Your score is near or slightly above the average of U.S. consumers and most lenders consider this a good score. |

| 740-799 | Very Good | Your score is above the average of U.S. consumers and demonstrates to lenders that you are a very dependable borrower. |

| 800+ | Exceptional | Your score is well above the average score of U.S. consumers and clearly demonstrates to lenders that you are an exceptional borrower. |

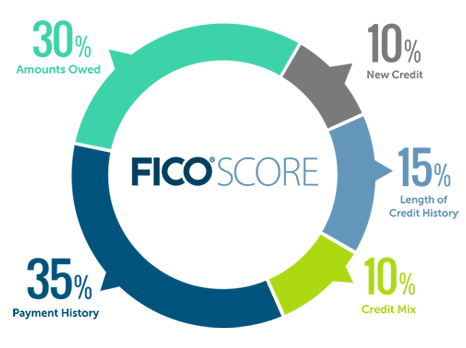

Be sure to keep your accounts in good standing to build a healthy history.

Having credit accounts and owing money on them does not necessarily mean you are a high-risk borrower with a low FICO Score. However, if you are using a lot of your available credit, this may indicate that you are overextended—and banks can interpret this to mean that you are at a higher risk of defaulting.

In general, a longer credit history will increase your FICO Scores. However, even people who haven't been using credit for long may have high FICO Scores, depending on how the rest of their credit report looks.

Your FICO Scores take into account:

FICO Scores will consider your mix of credit cards, retail accounts, installment loans, finance company accounts and mortgage loans. Don't worry, it's not necessary to have one of each.

Research shows that opening several credit accounts in a short amount of time represents a greater risk—especially for people who don't have a long credit history. If you can avoid it, try not to open too many accounts too rapidly.

The Secret History of the Credit Card:

https://www.pbs.org/video/frontline-the-secret-history-of-the-credit-card/

Contact Us Now For More Information

Your request has been submitted.